Grab: Potential Acquisitions

How Will Grab Spend $7.5 Billion?

Grab recently made headlines by upsizing its convertible note issuance to $1.5B from the previously announced $1.25B.

With this raise, Grab now has ~$7.5B in available cash to fund a variety of actions, including acquisitions, buybacks and internal expansion.

I wrote a short piece regarding my personal thoughts on the $1.5B raise recently:

Today, I would like to focus on the topic of acquisitions, particularly in light of growing market speculation around a potential mega-deal with GoTo. GoTo is Grab’s largest rival in Indonesia, a market that accounts for approximately 40 percent of Southeast Asia’s population.

However, I will also explore alternative targets, in light of Grab’s recent comments about the business not being in talks with GoTo “at this time”.

Here you can find a link to my post on my thoughts regarding recent rumours.

The stakes could not be higher. Grab’s markets are entering a new phase of consolidation, while rivals such as Sea Limited are scaling aggressively in adjacent verticals. At the same time, Grab’s balance sheet strength gives it rare flexibility at a moment when many regional players are capital-constrained.

Against this backdrop, with $7.5B in cash, Grab is now uniquely positioned to pursue several value-accretive acquisitions across its three core segments, as well as in adjacent verticals where it can further strengthen its ecosystem and competitive moat.

Table of Contents:

Mobility: GoTo & Regional Ride-Hailing Players

Deliveries: Food & Parcel

Financial Services: FinTech Expansion

Adjacent Vertical Opportunities

Risks and Constraints

Strategic Outlook

Conclusion

1. Mobility: GoTo & Regional Ride-Hailing Players

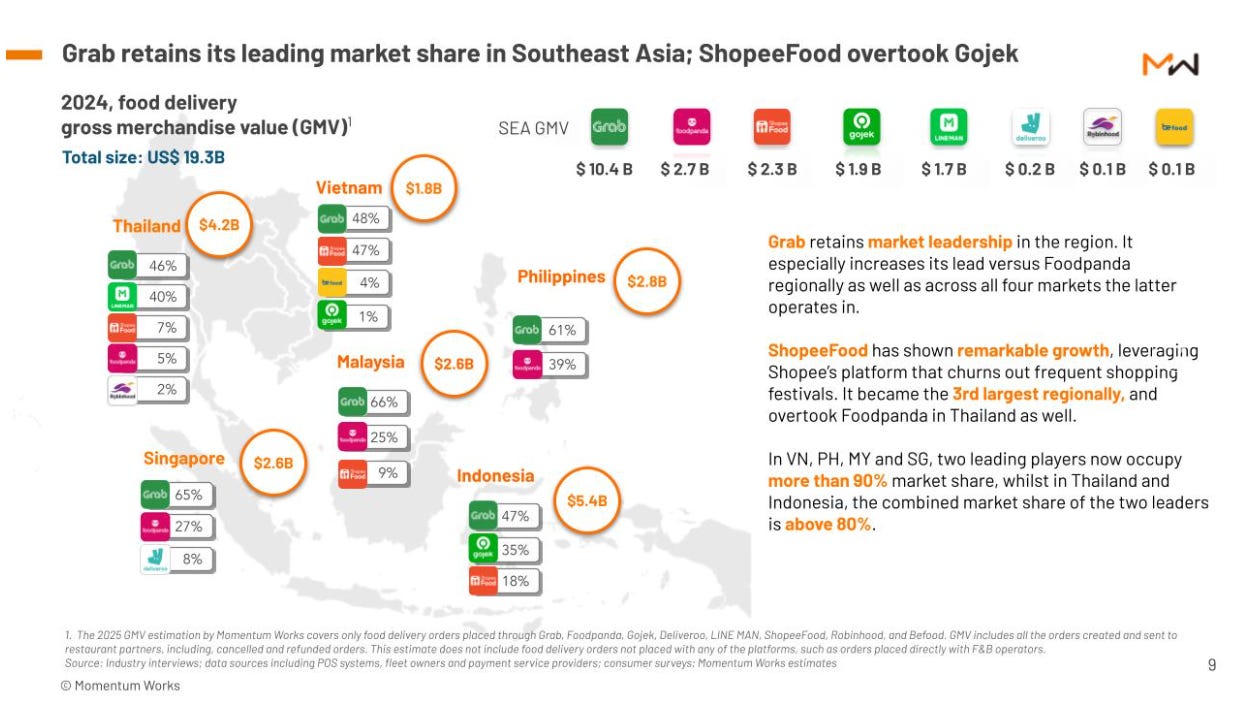

Grab is the dominant ride-hailing player in Southeast Asia with ~50% market share. However, as the company continues to spend hundreds of millions on incentives to sustain and grow its market share, acquiring its competitors to create an effective monopoly may prove to be the most straightforward solution.

GoTo (Gojek + Tokopedia)

The GoTo deal has been in talks for several years now, with a potential deal estimated at around $7B.

The deal would allow Grab to control over 90% of Indonesia and Singapore’s ride-hailing market, and ~85% of Southeast Asia’s ride-hailing volume.

As of today 13th June 2025, GoTo is trading at ~$4.5B, and I believe a deal could be made between $6 to $6.5B.

Personally, I think a deal between Grab and GoTo would be highly value accretive to the business; adding up to 10% in pro-forma NPV of the business, along with continued synergies for the next 5 years.

However, such a deal faces severe antitrust risk, regulators in Indonesia and Singapore would almost certainly scrutinise it closely.

Likelihood: Medium/High, although the timeline could be extended due to near-term regulatory and execution barriers.

Xanh SM (Vietnam)

Xanh SM is a taxi and ride-sharing company operating in Vietnam and was founded by the chairman of the Vingroup Corporation, a Vietnamese conglomerate that accounts for ~1.1% of Vietnam’s GDP.

Rakuten Insight estimates that Xanh SM is the second most frequently used ride-hailing player with 33% market share and Grab leading the way with ~55% share.

Mordor Intelligence estimates that Xanh SM is the leader in the Vietnamese ride-hailing market with 39% market share, and Grab with 35%.

Regardless of which source is used, it is clear that Xanh SM is a formidable player with strong backing.

Additionally, Xanh SM is also preparing to enter the food delivery segment through Xanh SM Ngon.

Likelihood: Low. Although this would be a great acquisition for Grab, it is unlikely that Vingroup would want to sell their prized asset.

Be Group (Vietnam)

It reportedly has ~20M users and last raised about $40M in funding from VPBank Securities and a ~$60M loan from Deutsche Bank.

Be Group has an estimated 9% market share and would help Grab to challenge Xanh SM for first place in Vietnam.

Likelihood: Medium. Be Group is the clear 3rd place and could potentially be looking for an exit, in a space that looks more likely than not to become a duopoly.

Ryde Technologies & Tada (Singapore)

Both are small players in Singapore with single digit market share that Grab could consider scooping up at a low price, likely below the $100M mark, and could work as simple bolt-on acquisitions to further consolidate its position.

Likelihood: Medium. Grab is the clear leader in Singapore, and while Ryde and Tada have some differentiation (e.g. Tada charges zero commission to drivers, only platform fees), it is hard to beat the dominant supply-demand flywheel that Grab and Gojek have built over the past decade.

Bolt (Thailand)

Bolt is an Estonian ride-hailing player and entered the Thai market in mid 2020 as the ride-hailing business was hit by the pandemic.

It is the second largest player with an estimated 30% market share, behind just Grab.

Likelihood: Medium. Bolt could look to sell and focus on its European operations.

Line Man (Thailand)

Line Man is the only domestic player in the Thai ride-hailing market. Its primary business is food delivery, but in Jan 2024 it expanded into ride-hailing and has since achieved notable success, with 60% growth reported by December 2024 and Line Man Bike growing by 390%.

The company plans to extend its coverage to all major Thai cities within the next 18 months.

As of May last year, Line Man was considering an initial public offering and is backed by several major investors, including Singapore’s sovereign wealth fund GIC and Z Holdings, a joint venture between SoftBank and South Korean internet firm Naver.

Likelihood: Medium. An acquisition appears plausible, particularly as SoftBank is a significant investor in both Grab and Line Man, and may favour a merger to prevent a prolonged competitive battle between its portfolio companies.

2. Deliveries: Food & Parcel

Grab’s deliveries segment is its largest segment by revenue and profitability, with an estimated 55% market share in Southeast Asia.

FoodPanda (Singapore, Malaysia, Philippines)

FoodPanda is the 2nd largest food delivery player in Southeast Asia and operates in 3 of the 6 Southeast Asian countries after recently ceasing operations in Thailand in May 2025.

Riyado Sofian, one of my favourite writers on X and Seeking Alpha recently published a thoughtful piece suggesting that FoodPanda is a likely acquisition candidate. I share this view and would encourage readers to explore his analysis.

FoodPanda is the fiercest competitor to Grab in the food delivery space. Notably, it attempted to sell its Taiwan operations to Uber in December last year, although the deal was ultimately terminated due to regulatory concerns.

Acquiring FoodPanda (~$2-3B) would consolidate Grab’s leadership in food delivery and create significant scale-driven margin expansion.

~1x Revenue Multiple @ 2024 Revenue of $2.7B

Likelihood: Medium to High. I believe FoodPanda is a likely candidate for acquisition.

Line Man (Thailand)

As mentioned previously, Line Man started off in the food delivery business and is actually the 5th largest player in Southeast Asia and a close second in Thailand with 40% market share, just behind Grab with 46%.

It would certainly spark antitrust reviews but would be a great acquisition for Grab if they could pull it off. I would estimate Line Man to cost ~$1B, making it well within reach for Grab.

Likelihood: Medium. (Reasons mentioned above)

Deliveroo (Singapore)

Deliveroo is a niche challenger to Grab and FoodPanda in Singapore and its reach is limited to a single market, with revenues estimated to be ~$200M (a mere 2% of Grab’s revenues in 2024)

Likelihood: Low. Given Deliveroo’s limited scale and market footprint, it is unlikely to be a priority acquisition target for Grab.

3. Financial Services: FinTech Expansion

GFin, with GrabPay, Lending, Insurance and its various DigiBanks, is now a major pillar of Grab. Its internal data (millions of gig workers and transactions) give it a clear edge in credit scoring, and is a key lever for differentiation in the increasingly saturated Southeast Asian FinTech market.

Future M&A here could include acquiring or investing in digital banks and fintechs that complement GrabPay. For example, Grab might seek stakes in or partnerships with leading e-wallets or digital lenders in markets it serves.

I will not be commenting on the likelihood here as these are pure speculative targets, and just some examples of the types of businesses Grab could acquire with the $7.5B cash pile in hand.

Validus Group

Earlier this year in April, Grab acquired Validus Group’s Singapore business for an undisclosed fee, in an all-cash deal. Market estimates place the deal value between $100M to $150M.

Following the acquisition, Validus Capital became a wholly-owned subsidiary of GXS Bank.

Validus Capital is an established SME lender that has disbursed over $1 billion in loans. The acquisition has broadened Grab’s SME lending capabilities, adding trade finance, supply chain finance and working capital solutions to its portfolio.

It is plausible that Grab may seek to acquire the entire Validus Group over time, positioning the Singapore transaction as a potential first step in a broader expansion strategy.

Timo (Vietnam)

Vietnam’s first digital-only bank (launched in 2015), offering digital spend accounts, term deposits, debit/credit, overdrafts, BNPL and insurance integrations.

An acquisition here would deepen GrabPay and GXS Bank’s reach into Vietnam’s underbanked and digitally savvy users. There would also be huge cross-sell synergy, integrating lending, savings, insurance and investing into Grab’s app.

BigPay (Malaysia)

BigPay is an AirAsia-backed neobank offering wallets, remittance, credit, debit cards, micro-loans and consumer payments.

This would help to strengthen Grab’s GXBank in Malaysia and expand user engagement and loyalty in the country.

UNO Digital Bank (Philippines)

Licensed digital bank offering savings accounts, deposits and loans.

UNO Digital Bank has partnered with the likes of Gcash and Singlife to introduce various products to consumers.

Grab does not currently have a Digital Bank in the Philippines and this could be a perfect segue way into the country, tapping into the huge unbanked population.

Funding Societies (Southeast Asia)

Funding Societies provides SME financing across 5 key markets in Southeast Asia; Singapore, Indonesia, Malaysia, Thailand, and Vietnam.

Since its inception, the company has provided over US$4 billion in financing to approximately 100,000 SMEs and processed an annualised gross transaction value of US$1.4 billion through its payments platform.

This will likely be a hefty fee, but one that could be highly value-accretive for Grab and position them to be a major player in the SME Lending space.

Crowdo (Southeast Asia)

Crowdo offers micro and working-capital loans in Indonesia, Malaysia and Singapore, matching SMEs with individuals and institutional lenders through digital credit scoring.

Crowdo’s invoice financing aligns closely with Validus' existing unsecured SME loans, perfect for expanding financial services for business clients.

While not asset-backed, their platform enables SMEs to secure invoices or digital collateral, broadening GXS’s SME financing range.

Presence in Grab’s core markets makes Crowdo a strategic partner for scaling SME finance via Grab’s DigiBanks and app.

Deals in the FinTech space would generally face fewer antitrust issues than ride-hailing or deliveries deals and could be equally value-accretive for Grab.

In my view, Grab is likely to invest in or acquire fintech assets that deepen its ecosystem (digital banks, remittance, wealth platforms) rather than pursue risky large takeovers in this domain.

4. Adjacent Vertical Opportunities

Beyond its core segments (mobility, delivery, fintech), Grab can leverage its Super App ecosystem to move into new verticals:

Logistics & Supply Chain:

GrabExpress and GrabMart already handle millions of parcels and grocery orders.

A logical move would be deeper logistics: e.g. acquiring warehouse/delivery startups or expanding last-mile delivery networks.

Ninja Van comes to mind here and would likely cost ~$1.5B to $2B.

Ad-Tech & Media:

GrabAds (its in-app advertising arm) grew by 60% YoY in Q4 2024 and was pacing at an annualised $216M run-rate. Grab may seek to bolster this by acquiring or partnering with digital marketing platforms.

Possible targets include regional ad-tech firms (programmatic DSPs, affiliate networks, or digital out-of-home media companies) that can integrate with GrabAds.

For instance, a startup managing street-level billboards or mobile ads could be folded into Grab’s ad stack. This would diversify revenue and help Grab monetise its large user base. Ad-tech deals would face relatively few regulatory barriers, though the strategic fit must be clear.

Autonomy:

Grab recently signed MOUs with 4 Autonomous Technology firms — Autonomous A2Z, Motional, WeRide and Zelos, to explore how AVs fit into Southeast Asia’s transportation ecosystem.

An acquisition of one of these firms could secure proprietary technology, that could be crucial as Grab prepares itself for the inevitable future.

Grab could also consider partnering or acquiring fleet management companies that operate logistics or delivery bots. Combining this hardware with existing software infrastructure that Grab possesses would enhance operational control and enable economies of scale.

“We believe we are in prime position in supporting the AV transition over the next few years via a hybrid AV human fleet … We are in active discussions with regulators” - Grab CEO Anthony Tan

5. Risks and Constraints

Grab’s ambitious M&A ambitions must navigate several constraints:

Regulatory Scrutiny:

Most SEA countries have active antitrust authorities (e.g. Singapore’s CCCS, Malaysia’s MyCC, Indonesia’s KPPU). Large deals that concentrate market power, especially if Grab already leads, are likely to be challenged.

Competition:

Grab faces fierce rivalry in acquisitions from a variety of players.

Sea Limited (Shopee/ShopeeFood) has deep pockets and may accelerate its delivery and fintech plays, possibly bidding on any divested assets (e.g. Sea reportedly considered acquiring Foodpanda).

Estonian Ride-Hailing Player Bolt has also entered Malaysia.

Chinese-backed firms (ByteDance/TikTok, Tencent) are increasingly interested in SEA’s digital economy.

Valuation and Funding:

Many target startups have sky-high valuations or are loss-making.

Grab’s bond proceeds and cash are large but not unlimited. Overpaying risks pressure on Grab’s own stock.

Investors will certainly be watching closely whether Grab finances deals with debt or equity and how quickly these acquisitions accrete value.

Integration Challenges:

Combining large technology companies (with different cultures, tech stacks, and legacy stakeholders) can be difficult. Grab historically has kept acquisitions relatively small.

A $7B GoTo deal, if attempted, would be a massive integration effort across fintech, ride-hailing and deliveries, that has a likelihood of backfiring.

Market Maturation:

In some segments, Grab already has very high share, allowing for limited growth ahead.

Grab must weigh expanding market share against the diminishing returns of saturating a mature market versus investing in new services or markets.

6. Strategic Outlook

In the next 3–5 years, Grab is likely to play selectively; using its war chest to “buy market share” where it can materially improve profitability and reinforce leadership, while avoiding fights that risk all.

High-probability moves include bolt-on acquisitions in fintech (e.g. digital banks, e-wallets, micro-finance), where Grab’s data and platform can easily integrate new offerings. Although these transactions face regulatory scrutiny, they generally do not attract the same level of antitrust concern as deals in the mobility sector.

Medium-probability targets include smaller mobility and delivery players in specific markets, such as Be Group, Line Man and Bolt, as well as potential stakes in logistics firms. GoTo also falls within this category; while market speculation suggests a deal is likely, significant antitrust risks remain a major hurdle.

Low-probability targets comprise established players with strong market positions and deep backing from institutional investors or wealthy individuals, such as Xanh SM. Given their robust funding and long-term ambitions, these companies are unlikely to consider an outright sale to Grab in the near term.

7. Conclusion

Armed with $7.5B in liquidity, Grab is well-positioned to pursue strategic M&A in Southeast Asia. In my view, its likely path is a mix of expansion in high-growth adjacent areas and opportunistic deals to squeeze out the remaining competition.

The success of this strategy will depend on regulatory outcomes and Grab’s ability to integrate acquisitions efficiently. For investors, the key questions are whether Grab can use its war chest to defend or extend its competitive advantages, driving higher margins and profitability while looking to limit regulatory pushback.

Overall, I believe Grab’s recent issuance of convertible debt, despite already having $6B in the bank suggests a willingness and immediate appetite to spend big for market leadership. I believe we are in for an exciting few quarters ahead in terms of acquisitions.

Thank you for reading.

This is the kind of in-depth content that will be regularly available to paid subscribers. I chose to share this piece publicly today, as several readers had asked about the type of insights included in the paid tier.

As I have mentioned in earlier posts, I will be officially launching the paid subscription later this month. The current rate is an early-bird offer for those who choose to support the publication at this stage.

The next piece, exclusively for paid subscribers, will feature a comprehensive analysis of Grab’s past acquisitions. I will explore their acquisition strategy in detail and discuss key lessons we can draw from their approach.

For free subscribers, rest assured that the majority of content will remain freely accessible, and I remain committed to delivering valuable insights and content.

What about deals to enter new geographies? India, Sri Lanka, Bangladesh, Pakistan or other?